IPO Notes # 2 : Stove Kraft

Can the "Pigeon" fly high? A 20 year old player in the highly competitive kitchen appliances market taking steps towards premiumization.

Dear Reader,

Thanks for opening this post. Congratulations ! You have take the first step towards understanding this business and industry if you are new to this sector (like me!)

If you are a seasoned investor, I hope that you find something new to learn by the end of this post.

I have learned immensely from great investing legends and teachers from the internet & twitter ( note that Learning!= Success) and this medium is my way of paying it forward to the investing community at large. So catch a cup of coffee and start scrolling!

There are high chances of you spending more time than usual in your kitchen during this Covid induced lockdown . If you have used or searched for any kitchen appliance online/offline, you might have heard of “Pigeon” brand. In this letter, we will delve into the IPO filing of StoveKraft ( company behind the “Pigeon and Gilma” brands)

IPO Filings/DRHP’s are some of the best places to learn from when you are trying to understand the company and industry it operates in.

NOTE: Below notes are based on the filed Stove Kraft IPO prospectus , please consult your financial advisor for advice before investing in any financial product. Please also note that I am not a SEBI registered investment advisor, these articles are for learning purpose only and should not be considered as investment advice.

Introduction

The company Stovekraft was incorporated in June , 1999

It has grown from a single brand small LPG stove manufacturing company to become one of India’s leading manufacturers of kitchen appliances

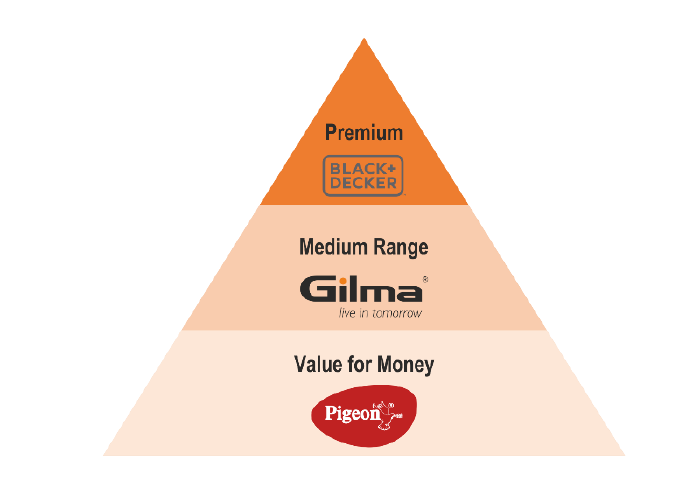

Engaged in the manufacture and retail of a wide and diverse suite of kitchen solutions under Pigeon and Gilma brands, and proposes to commence manufacturing of premium kitchen solutions under the BLACK +DECKER brand.

The BLACK+ DECKER Brand is under a trademark license agreement with Stanley Black & Decker, Inc. and The Black and Decker Corporation for purpose of manufacturing, distributing, marketing and selling blenders and juicers, breakfast appliances, small cooking appliances and small domestic appliances in India( which are not in the current portfolio of the company)

Kitchen solutions comprise of cookware and cooking appliances, and home solutions comprise various household utilities, including consumer lighting,

While historically it was a manufacturer and retailer of kitchen appliances, it entered the LED market in 2016 under Pigeon Brand .

IPO

The objective of the IPO is to raise fresh capital and also provide partial exit to existing shareholders and promoters

Company aims to raise fresh capital raise of 145 Cr

It plans to use the raised funds to repay borrowings of 110 Cr and general corporate purposes.

Drivers for the growth of consumer appliances industry

The growth in the Kitchen appliances market is expected to be driven by the following:

Increasing per capita income (leading to higher disposable income)

Increasing middle class segment

Shift from ‘Unorganized’ to ‘Organized’ Sector

Increasing residential electricity consumption in Indian Households

Growth of E-commerce and easy financing options

Aspirations for lifestyle appliances,

Competitive Landscape

StoveKraft operates in the highly competitive market of kitchen appliances with host of multiple entrenched competitors like TTK Prestige, Hawkins, Bajaj Electricals, Preethi Industries Ltd., Glen, Faber, Kaff Appliances, Inalsa, IFB, Panasonic, and Phillips etc.

Please note that RSV is the Retail sales volume in the above table

StoveKraft is a market leader only in the Cooking Hobs and Cooktops category and has a small market share in all the other categories it operates in.

Has co-branding initiatives of over 7 years with LPG companies such as Indian Oil Company Limited and Hindustan Petroleum Corporation Limited to utilize their sale and distribution channels aided by Pradhan Mantri Ujjwala Yojana

TTK Prestige is the largest listed peer with annual revenues ~1900 Cr and Market cap of 7400Cr+

Source: FY19 Annual reports of companies

As we can see from the above comparison table, Hawkins and Butterfly Gandhimathi have a similar scale of revenues around 650 Cr.

StoveKraft has been improving its EBITDA margins, and we can see an major improvement in HY20 over FY19. The profitability margin is also improving YoY .

The inventory turnover ratio is also close to the average in the industry. Given that the low capacity utilization currently at both of its plants, we can expect the StoveKraft’s operating leverage to kick in once the sales increase.

News reports indicate Stovekraft seeking a 1500-2000 Cr valuation ( In line with market cap to sales of 3.7x-3.8x). The median 5 year PE for the listed peers is as follows: Hawkins: 31 , Butterfly : 31 , TTK Prestige: 49.

Please note that the kitchen appliances market is a highly competitive market with multiple players - refer to the snippets from credit rating reports of TTK Prestige and Butterfly Applicances below

Source: TTK Prestige Crisil Credit Rating Report July 2020

Source: ICRA Butterfly Gandhimathi Appliances Limited Credit Report June 2020

Business Overview

StoveKraft is one of the leading brands for kitchen appliances in India, and are one of the dominant players for pressure cookers and amongst the market leaders in the sale of free standing hobs and cooktops

It’s brands, Pigeon and Gilma, have enjoyed a market presence of over 14 years

Manufactures and retails a wide and diverse range of affordable (value segment), quality products under Pigeon brand, including, inter alia, cookware, cooking appliances and household utilities (including consumer lighting).

Also offer a wide range of products such as chimney, hobs and cooktops under the Gilma brand, which is targeted at the semi-premium segment.

Entered the premium segment in 2016 by the exclusive BLACK + DECKER Brand Licensing Agreement which enables it to exclusively retail, and provide post -sales services for wide range of products such as blenders and juicers, breakfast appliances, small cooking appliances and small domestic appliances. The License Agreement is valid up to December 31, 2027. For each contract year, StoveKraft is required to pay B&D royalties at a fixed rate on all total sales of licensed products. Further, for the first 10 contract years, B&D is also entitled to guaranteed minimum royalty payments

As of October 31, 2019, it manufactures 68.60% of Pigeon and Gilma branded products (in terms of number of units) at integrated manufacturing facilities at Bengaluru (Karnataka) and Baddi (Himachal Pradesh)

Bengaluru Facility : Spread over approximately 40 acres and 16 guntas, out of which 27 acres and 22 guntas is available for future expansion. As of October 31, 2019, it had an installed annual production capacity of 19.50 million units, comprising of nine manufacturing units- pressure cookers, non -stick cookware (roller coated and spray coated), LPG stoves, mixer grinders, LED bulbs, iron and induction cooktops categories. Capacity utilization of 29%

Baddi Facility: Operational from 2005, focused on the Oil Company Business, which includes manufacturing and co-branding of products with such Companies has an installed capacity of 2.8 million units per annum, with the capability to manufacture products such as LPG stoves and inner lid cooker. Baddi Facility benefits from its strategic location, as most LPG stove manufacturers are located in northern India which enables the facility to source raw material and skillful resources in an efficient manner.Capacity utilization of 14%

For certain product categories and sub-categories ( such as chimneys, hobs, irons, air coolers, kettles, water bottles, flasks, chairs, rice cookers, etc.,) which do not enjoy economies of scale in India, StoveKraft sources from third party OEMs from China . For Fiscal 2019, such products contributed 31.40% to our turnover, as compared to 29.60% for Fiscal 2018.

Distribution Network

3 strategically located C&F agents.

429 distributors in more than 24 states of India

10 distributors for exports , sold in to 12 countries including UAE, Qatar, Bahrain, Kuwait, Iran, Tanzania, Uganda, Nepal, Philippines, Sri Lanka, the United Kingdom and the Netherlands. Exports contributed 8.67% of sales in FY19

C&F agents and distributors connected with a dealer network comprising of over 38,090 retail outlets

Sales force of 701 personnel.

62 Gilma exclusively branded franchisee outlets spread across five states and 28 cities, with a presence in the urban market in south India

Employee Base

Also engages contract labourers to facilitate our manufacturing operations. As of October 31, 2019, it engaged 441 contract workers.

Financials

Company grew its revenues at a CAGR of 11.4% between FY17-19 from 517 Cr to 642 Cr.

Given the majority of the sales is driven by the Pigeon brand catering to the affordable, price sensitive,value conscious segment, the shift towards portfolio premiumization via Gilma and B & D is a good strategy.

The revenue under the Gilma brand is lower than the previous fiscal as the company continues to restructure the business.

Do note that even TTK Prestige has ventured into the luxury kitchen segment in categories such as dishwashers, built-in ovens and island chimneys through Prestige Lifestyle stores!

Company is spending lesser on advertisements/promotions as compared to other listed peers -> Note that Butterfly which is strong in southern market with similar core product portfolio spends more than StoveKraft. This probably indicates of strong brand presence - investments may give a multiplier boost to the topline.

Company has cash and bank balances of 10 Cr as of Sep 2019

Company has short term and long term borrowings of 162 Cr as of Sep 30th, 2019 and contingent liabilities of 14.7 Cr

As of October 31, 2019, it had 2,868 permanent employees engaged across various operational and business divisions in India.

Risks

Brand: The brand name “Pigeon” is under dispute with an associate company , Pigeon Appliances Private Limited (PAPL) . In 2003, PAPL was allowed to use the brand name to manufacture certain products (mixers and grinders) based on an oral understanding . StoveKraft had initiated legal action against PAPL for irregularities noted in the business operations and unauthorized use of trademarks. It had filed a suit in 2015 to bar PAPL from usage of its brand , which the court had granted a temporary injunction through which PAPL is retrained from using the “Pigeon” trademark. The matter is currently pending. Given that Pigeon brand sales contribute to ~80%+ of sales, this is an risk factor. Please note that Promoter and Managing Director, Rajendra Gandhi, is one of the directors on the board of PAPL and StoveKraft owns 37.4% of PAPL. (more details are available at page 248 of the DRHP)

Sourcing: The company is significantly dependent on local third parties for all stages of product development and sales. The principal raw materials ( glasses components, aluminum, steel) come from foreign suppliers and local materials are sourced from third parties

Group company in same line of business: A Group company, SAEPL is engaged primarily in the business of manufacturing, importing and exporting of components for domestic and other appliances such as heating stoves for domestic application and jugs for consumer durables, a line of business similar to Stovekraft. There is no non compete agreement with StoveKraft

Geographic concentration: Nearly 60% of total revenues are from the southern Indian states, with all the 62 Gilma branded franchisee stores located in South India. Expanding the sales to other parts of the country will need to be monitored

Shareholders

Sequioa Capital is an investor in the company since 2010 (Via SCI and SCI-GH)

Offer for sale is for 7,163,721 Equity Shares comprising of

640,906 Equity Shares by Promoter, Rajendra Gandhi,

250,000 Equity Shares by Promoter, Sunita Rajendra Gandhi,

1,311,205 Equity Shares by SCI-GIH

4,961,610 Equity Shares by SCI

This is in addition to the 145 Cr fresh capital to be raised by the company through fresh issue of shares.

Comments:

The company seems to be on the right track towards shifting the portfolio towards semi premium /premium products which should aid in improving the portfolio margins. The decision of outsourcing the manufacturing of products which currently doesn’t have economies of scale also seems to be a right decision. There can be a improvement in profitability once the operating leverage kicks in.

Do let us know your feedback on the note. Happy Learning!

Disclaimer: Please consult with your financial advisor before taking any investment decision. I am not a SEBI registered investment advisor and this note should not be considered as an investment advice.

The Company is not helping itself by not advertising. Considering that the industry is highly competitive and also includes unbranded players, who hold significant position, innovation in the product range is a must. Further, the reason for which the company is raising funds is to settle another obligation, meaning, new funds aren't going to expand capacities or bring a change in portfolio however management could have it's own plan.